This is part 5 of the Math Foundations series.

The CLT gave us the sampling distribution - the sample mean is approximately normal, centred at $\mu$, with spread $SE = s / \sqrt{n}$. This post turns that into a decision-making framework: how to state a claim, test it against data, quantify uncertainty, and plan how much data you need.

Hypothesis Testing

Null and Alternative Hypotheses

Every hypothesis test starts with two competing statements about a population parameter.

Null hypothesis ($H_0$): the default claim. Usually “no effect” or “no difference.”

Alternative hypothesis ($H_1$): what you’re trying to find evidence for.

$$H_0: \mu = \mu_0 \quad \text{vs.} \quad H_1: \mu \neq \mu_0$$The logic is indirect. You don’t prove $H_1$ - you ask whether the data are unlikely enough under $H_0$ to reject it.

One-Sided vs Two-Sided Tests

The alternative hypothesis determines where you look for evidence against $H_0$:

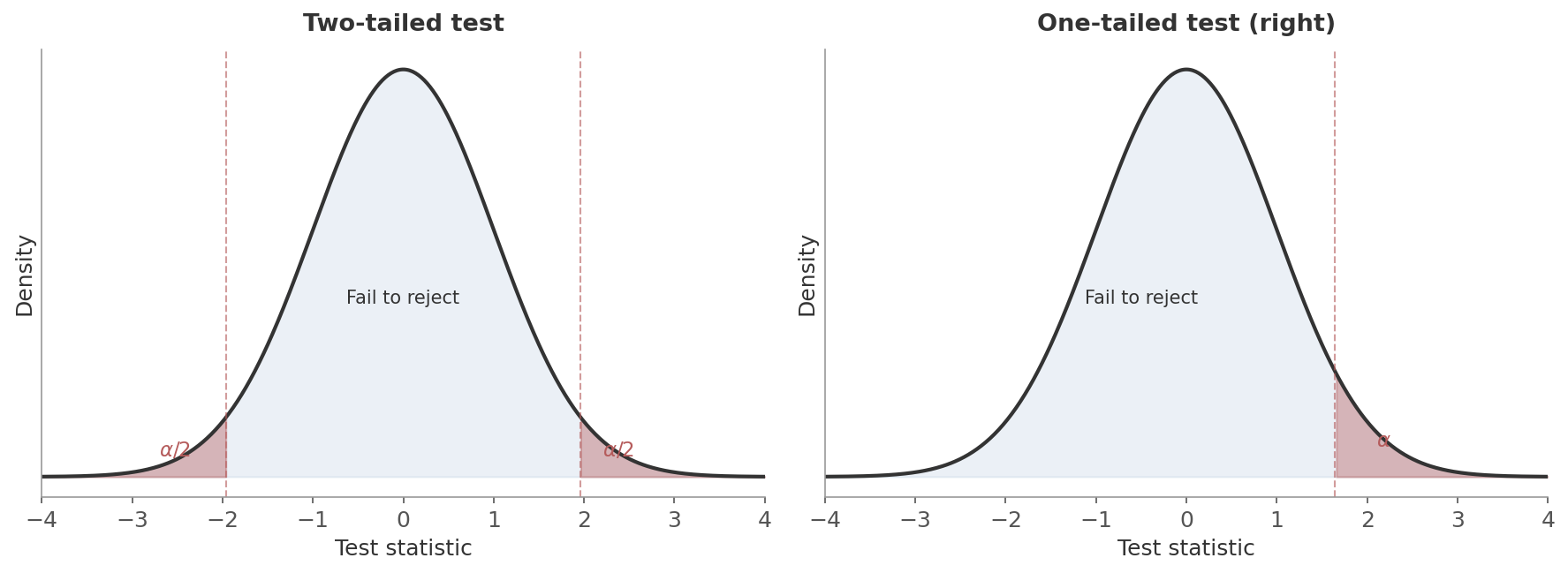

- Two-sided (two-tailed): $H_1: \mu \neq \mu_0$. Reject if the test statistic falls in either tail. The rejection region is split: $\alpha/2$ in each tail.

- One-sided (one-tailed): $H_1: \mu > \mu_0$ or $H_1: \mu < \mu_0$. All of $\alpha$ goes into one tail - easier to reject in that direction, but you can’t detect effects in the other.

Figure 1: Two-tailed (left) vs one-tailed (right) rejection regions. The red shaded areas are the rejection regions - if the test statistic lands there, you reject $H_0$. A two-tailed test splits $\alpha$ across both tails; a one-tailed test puts all of $\alpha$ in one tail.

Figure 1: Two-tailed (left) vs one-tailed (right) rejection regions. The red shaded areas are the rejection regions - if the test statistic lands there, you reject $H_0$. A two-tailed test splits $\alpha$ across both tails; a one-tailed test puts all of $\alpha$ in one tail.

Use two-sided unless you have a strong reason to only care about one direction before seeing the data. In A/B testing, for instance, you often use one-sided because you only care whether the variation is better than the control. But if a change could make things worse and you want to detect that too, use two-sided.

Test Statistics

A test statistic converts your data into a single number that you can compare against a known distribution. The idea: if $H_0$ is true, this number should look like a typical draw from that distribution. If it’s unusually far out, $H_0$ is in trouble.

- Numerator: how far the sample mean is from the hypothesised value

- Denominator: the standard error - expected sampling variability

- Ratio: how many standard errors away from $\mu_0$ your data landed

with degrees of freedom:

$$df = \frac{\left(\frac{s_1^2}{n_1} + \frac{s_2^2}{n_2}\right)^2}{\frac{(s_1^2/n_1)^2}{n_1 - 1} + \frac{(s_2^2/n_2)^2}{n_2 - 1}}$$Same logic: difference in means divided by the standard error of that difference. The $df$ formula (Welch-Satterthwaite) looks messy but it just accounts for potentially unequal variances and sample sizes.

For comparing two proportions (e.g. conversion rates in an A/B test), pool them under $H_0$:

$$z = \frac{\hat{p}_1 - \hat{p}_2}{\sqrt{\hat{p}(1 - \hat{p})\left(\frac{1}{n_1} + \frac{1}{n_2}\right)}} \quad \text{where } \hat{p} = \frac{x_1 + x_2}{n_1 + n_2}$$- $x_1, x_2$: number of successes (e.g. conversions) in each group

- $\hat{p}$: pooled proportion - overall success rate across both groups, used because under $H_0$ we assume the two proportions are equal

Same structure as the t-statistic: observed difference divided by standard error.

For means, use the t-test. It handles unknown population variance (which is almost always the case), and with large $n$ the t-distribution converges to the normal anyway. You lose nothing by defaulting to t.

For proportions, use the z-test. The variance under $H_0$ is fully determined by $p_0$ (since $\text{Var} = p_0(1-p_0)/n$), so there’s no unknown variance to estimate. The z-test is the standard choice.

P-Values

The p-value is the probability of observing a test statistic as extreme as (or more extreme than) the one you got, assuming $H_0$ is true.

- Two-sided: $p = P(|T| \geq |t_{obs}| \mid H_0)$ - extreme in either direction

- One-sided: $p = P(T \geq t_{obs} \mid H_0)$ - extreme in one direction only

The logic, step by step:

- Assume there’s no real effect ($H_0$ is true)

- Under that assumption, the CLT tells you what the sampling distribution looks like

- Compute where your data falls on that distribution

- The p-value is the probability of landing that far out or farther

A small p-value means your data would be unusual if $H_0$ were true - which is evidence against $H_0$.

A friend hands you a coin and claims it’s fair. You’re not so sure, so you flip it 10 times and get 9 heads. Should you believe your friend?

Take their claim as the null hypothesis:

- $H_0$: the coin is fair ($p = 0.5$)

- $H_1$: the coin is not fair ($p \neq 0.5$)

If your friend is right, the number of heads $X$ follows $\text{Binomial}(10, 0.5)$. The p-value asks: how likely is a result this extreme or more, if the coin really is fair? You got 9 heads, so $P(X \geq 9) = P(X = 9) + P(X = 10)$. But since you’d be equally suspicious of 9 tails, this is a two-sided test - you also count the mirror extreme, $P(X \leq 1) = P(X = 0) + P(X = 1)$. By symmetry of the fair coin, both tails are equal:

$$p = P(X \leq 1) + P(X \geq 9) = 2 \times \frac{\binom{10}{9} + \binom{10}{10}}{2^{10}} = 2 \times \frac{10 + 1}{1024} \approx 0.021$$Only about 2% of the time would a fair coin produce something this lopsided. At $\alpha = 0.05$, you’d reject your friend’s claim. You haven’t proven the coin is biased - but the data is hard to explain if it’s fair.

- The probability that $H_0$ is true. It’s $P(\text{data} \mid H_0)$, not $P(H_0 \mid \text{data})$.

- The probability the result happened “by chance.” It’s the probability of data this extreme under a specific null model.

- A measure of effect size. A tiny difference can produce a small p-value with enough data. A large difference can produce a large p-value with too little.

Significance Level and Decisions

The significance level $\alpha$ is the threshold you set before looking at the data.

- If $p \leq \alpha$: reject $H_0$

- If $p > \alpha$: fail to reject

The standard choice is $\alpha = 0.05$ - a 5% chance of a false positive. The connection to confidence intervals: $\alpha = 1 - \text{confidence level}$, so 95% CI $\leftrightarrow$ $\alpha = 0.05$.

Type I and Type II Errors

A hypothesis test can be wrong in two ways:

Type I error (false positive):

- You reject $H_0$ when it’s actually true

- The coin is fair, you just got an unlucky streak

- Probability: $\alpha$

Type II error (false negative):

- You fail to reject $H_0$ when it’s actually false

- The coin is biased, but your 10 flips weren’t extreme enough to catch it

- Probability: $\beta$

Think of a fire alarm. Positive/negative refers to the alarm (did it go off or not), false means it was wrong:

- False positive: alarm goes off, no fire. You “detected” something that isn’t there.

- False negative: no alarm, building is on fire. You missed something real.

Failing to reject $H_0$ means the data didn’t provide strong enough evidence against it. It doesn’t mean $H_0$ is true. You might simply not have enough data. Think of it like a jury verdict: “not guilty” doesn’t mean “innocent” - it means the evidence didn’t meet the standard.

Worked Example - One-Sample t-Test

A website’s historical average session duration is $\mu_0 = 30$ minutes. After a redesign, you sample $n = 50$ sessions and observe $\bar{x} = 33.2$ minutes with $s = 12.5$ minutes. Did the redesign change session duration?

Step 1: State hypotheses.

$$H_0: \mu = 30 \quad \text{vs.} \quad H_1: \mu \neq 30$$(Two-sided - the redesign could increase or decrease duration.)

Step 2: Compute the test statistic.

$$t = \frac{33.2 - 30}{12.5 / \sqrt{50}} = \frac{3.2}{1.768} = 1.81$$Step 3: Find the p-value. With $df = 49$ and a two-tailed test:

$$p = 2 \times P(t_{49} > 1.81) = 2 \times 0.038 = 0.076$$Step 4: Decide. At $\alpha = 0.05$: $p = 0.076 > 0.05$, so we fail to reject $H_0$. The data don’t provide sufficient evidence that the redesign changed session duration.

Note: at $\alpha = 0.10$, we would reject. The threshold matters.

Confidence Intervals

The CLT post covered the mechanics - the formula, the visualization, what “95% confidence” means across repeated samples. This section adds what that post didn’t: interpretation pitfalls, what controls width, and the connection to hypothesis testing.

Interpretation

“If we repeated this sampling procedure many times, about 95% of the resulting intervals would contain the true parameter.”

“There’s a 95% probability that the true value is in this interval.”

The difference is subtle but real. Once you’ve computed the interval, the true parameter is either in it or it isn’t - there’s no probability involved. The “95%” refers to the long-run success rate of the procedure, not to any single interval.

What Controls CI Width

Three levers determine how wide a confidence interval is:

where $t^*$ is the critical value for the chosen confidence level (e.g. $t^* \approx 1.96$ for 95% with large $n$).

- Sample size ($n$): more data $\to$ smaller SE $\to$ narrower CI. The $\sqrt{n}$ means diminishing returns - quadruple the data to halve the margin.

- Variability ($s$): noisier data $\to$ wider CI. You can’t control this, but you can sometimes reduce it with better measurement or stratification.

- Confidence level: higher confidence $\to$ wider CI. A 99% interval is wider than a 95% interval from the same data. You’re casting a wider net to be more sure you catch the true value.

CIs and Hypothesis Tests Are the Same Thing

A confidence interval and a hypothesis test answer the same question from different angles:

- Hypothesis test: can I reject this specific value?

- Confidence interval: here are all the values you can’t reject

The 95% CI is $\bar{x} \pm 1.96 \times SE$:

- $\mu_0$ inside the interval $\to$ $p > 0.05$ $\to$ can’t reject

- $\mu_0$ outside the interval $\to$ $p \leq 0.05$ $\to$ reject

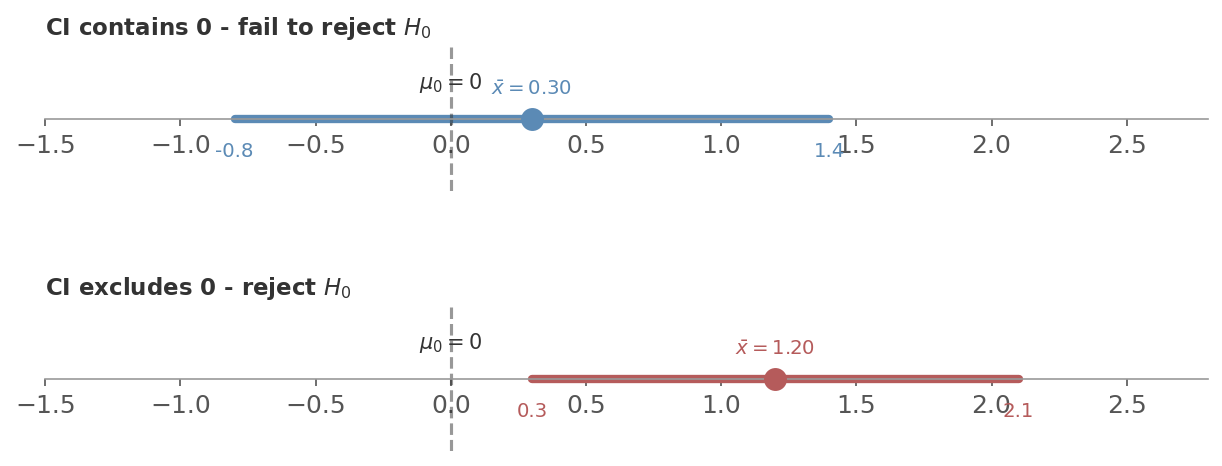

Say you’re testing whether a new feature changes average session time ($H_0: \mu_1 - \mu_2 = 0$). You compute the 95% CI for the difference:

- CI is $[-0.8, 1.4]$: contains 0. No effect is a plausible value - can’t reject $H_0$.

- CI is $[0.3, 2.1]$: excludes 0. Every plausible value is positive - reject $H_0$. The effect is somewhere between 0.3 and 2.1.

Figure 2: The CI-hypothesis test duality. Top: the 95% CI $[-0.8, 1.4]$ contains 0, so we fail to reject $H_0$. Bottom: the CI $[0.3, 2.1]$ excludes 0, so we reject $H_0$. Same information, two views.

Figure 2: The CI-hypothesis test duality. Top: the 95% CI $[-0.8, 1.4]$ contains 0, so we fail to reject $H_0$. Bottom: the CI $[0.3, 2.1]$ excludes 0, so we reject $H_0$. Same information, two views.

This is why many statisticians prefer reporting CIs over p-values. A p-value tells you “significant or not.” A CI tells you that and gives the plausible range of the true effect - something the p-value alone doesn’t give you.

CIs and Power

The width of a confidence interval tells you how much power you have. The chain works like this:

- The 95% CI is $\bar{x} \pm 1.96 \times SE$, and $SE = s / \sqrt{n}$

- Wide CI = large uncertainty. If the true effect is small, the interval will probably still contain 0 - you’ll miss it. That’s low power.

- Narrow CI = high precision. Even a small true effect pushes the interval away from 0. That’s high power.

- More data shrinks $SE$, which narrows the CI, which increases power.

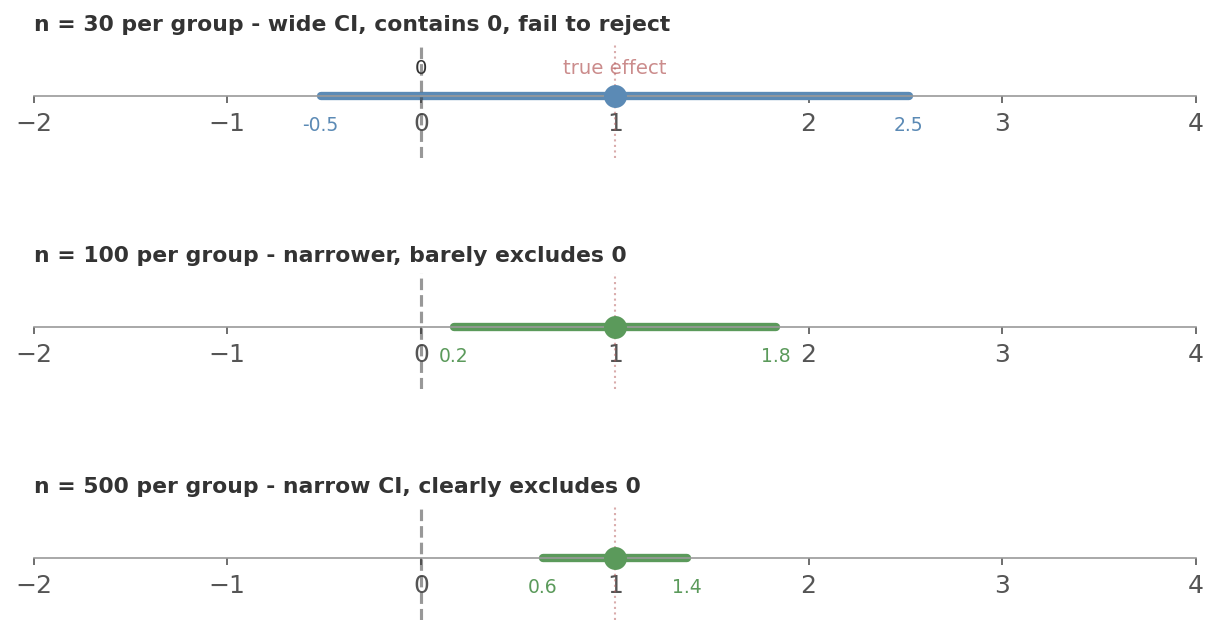

Back to the session-time example. Say the true effect of your new feature is a 1-minute increase ($\sigma = 3$). Watch what happens as you increase the sample size:

Figure 3: The same true effect (dotted red line), three different sample sizes. With $n = 30$ per group the CI (blue) is wide enough to contain 0 - you fail to reject and miss the real effect. At $n = 100$ the CI (green) barely excludes 0. At $n = 500$ it’s narrow and clearly excludes 0. The effect didn’t change. Your precision did.

Figure 3: The same true effect (dotted red line), three different sample sizes. With $n = 30$ per group the CI (blue) is wide enough to contain 0 - you fail to reject and miss the real effect. At $n = 100$ the CI (green) barely excludes 0. At $n = 500$ it’s narrow and clearly excludes 0. The effect didn’t change. Your precision did.

In short: wider CI means lower power, narrower CI means higher power. Collecting more data does both at once - it shrinks the CI and increases the probability of detecting a real effect.

Power Analysis and Sample Size

Statistical Power

Power is the probability of correctly rejecting $H_0$ when it’s actually false - detecting a real effect when one exists.

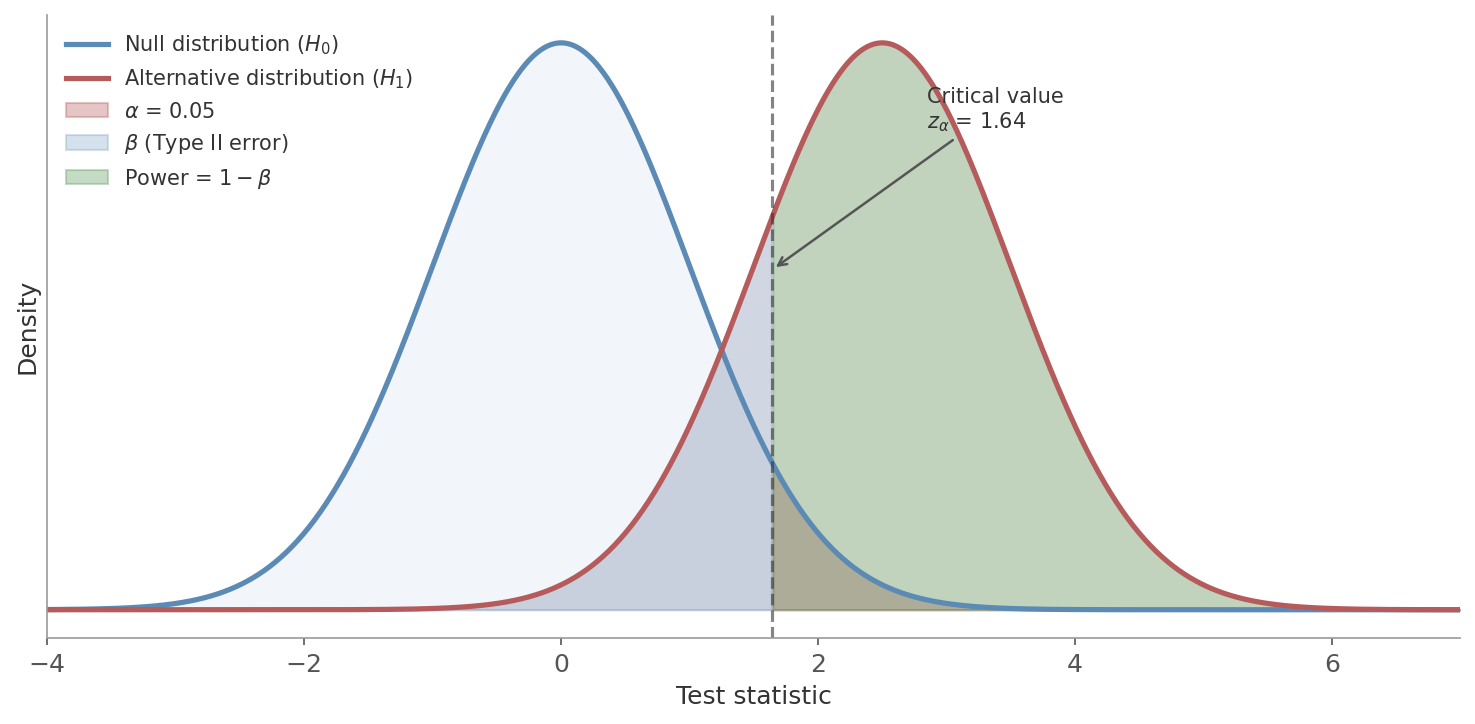

$$\text{Power} = 1 - \beta = P(\text{reject } H_0 \mid H_1 \text{ is true})$$The convention is to aim for power $\geq 0.80$, meaning at least an 80% chance of detecting the effect if it’s real. That still leaves a 20% chance of missing it.

Figure 4: The canonical power diagram. The blue curve is the sampling distribution under $H_0$ (no effect). The red curve is the distribution under $H_1$ (real effect of size $d$). The dashed line is the critical value. The red shaded area in the right tail of the null is $\alpha$ (Type I error). The blue shaded area to the left of the critical value under the alternative is $\beta$ (Type II error - failing to detect a real effect). The green area is power: the probability of correctly rejecting $H_0$ when the effect is real.

Figure 4: The canonical power diagram. The blue curve is the sampling distribution under $H_0$ (no effect). The red curve is the distribution under $H_1$ (real effect of size $d$). The dashed line is the critical value. The red shaded area in the right tail of the null is $\alpha$ (Type I error). The blue shaded area to the left of the critical value under the alternative is $\beta$ (Type II error - failing to detect a real effect). The green area is power: the probability of correctly rejecting $H_0$ when the effect is real.

Two ways to increase power (green area):

- Larger effect - moves the alternative distribution further right

- Larger $\alpha$ - moves the critical value left, but at the cost of more false positives

Effect Size

The raw difference between means depends on the scale of measurement - a 2-point difference means something different for SAT scores than for a 5-point survey. Effect size standardises this by dividing by the standard deviation.

where $s_p$ is the pooled standard deviation. Cohen’s conventions:

| $d$ | Interpretation |

|---|---|

| 0.2 | Small |

| 0.5 | Medium |

| 0.8 | Large |

These are rough guidelines, not rules. A “small” effect in one context can be practically important in another.

In A/B testing, you don’t usually think in terms of Cohen’s $d$. Instead, you specify the minimum detectable effect - the smallest difference that would be practically meaningful. “We want to detect at least a 2 percentage point increase in conversion rate.” The MDE is the same idea as effect size, just in the original units rather than standardised.

The Four-Way Trade-off

Four quantities are linked: $\alpha$, power, effect size, and sample size. Fix any three and the fourth is determined.

- Want to detect smaller effects? You need more data.

- Want higher power? You need more data (or accept a larger $\alpha$).

- Want a stricter $\alpha$? You need more data (or accept lower power).

The sample size formula for a two-sample test (equal groups) makes this explicit:

- $\delta$: minimum detectable difference

- $s$: assumed standard deviation

- $z_{\alpha/2}$: critical value for the significance level

- $z_{\beta}$: critical value for the desired power

You’re planning an A/B test on session duration. Current average is 30 minutes with $s = 18$ minutes. You want to detect a 3-minute increase ($\delta = 3$) with 80% power at $\alpha = 0.05$.

- $z_{\alpha/2} = z_{0.025} = 1.96$ (two-tailed)

- $z_{\beta} = z_{0.20} = 0.84$ (80% power)

You need roughly 565 users per group - 1,130 total. If that’s more than you can get in a reasonable time:

- Accept lower power

- Accept a larger MDE

- Find ways to reduce variance

What Happens When You Skip Power Analysis

- Underpowered (sample too small): you’re unlikely to detect real effects. You get $p > 0.05$ and conclude “no effect” - but really you just didn’t have enough data. Waste of time and traffic.

- Overpowered (sample too large): you detect effects too small to matter. A 0.1-minute increase might be “significant” with $n = 100{,}000$ per group, but nobody cares about 6 extra seconds. Waste of traffic that could go to the next experiment.

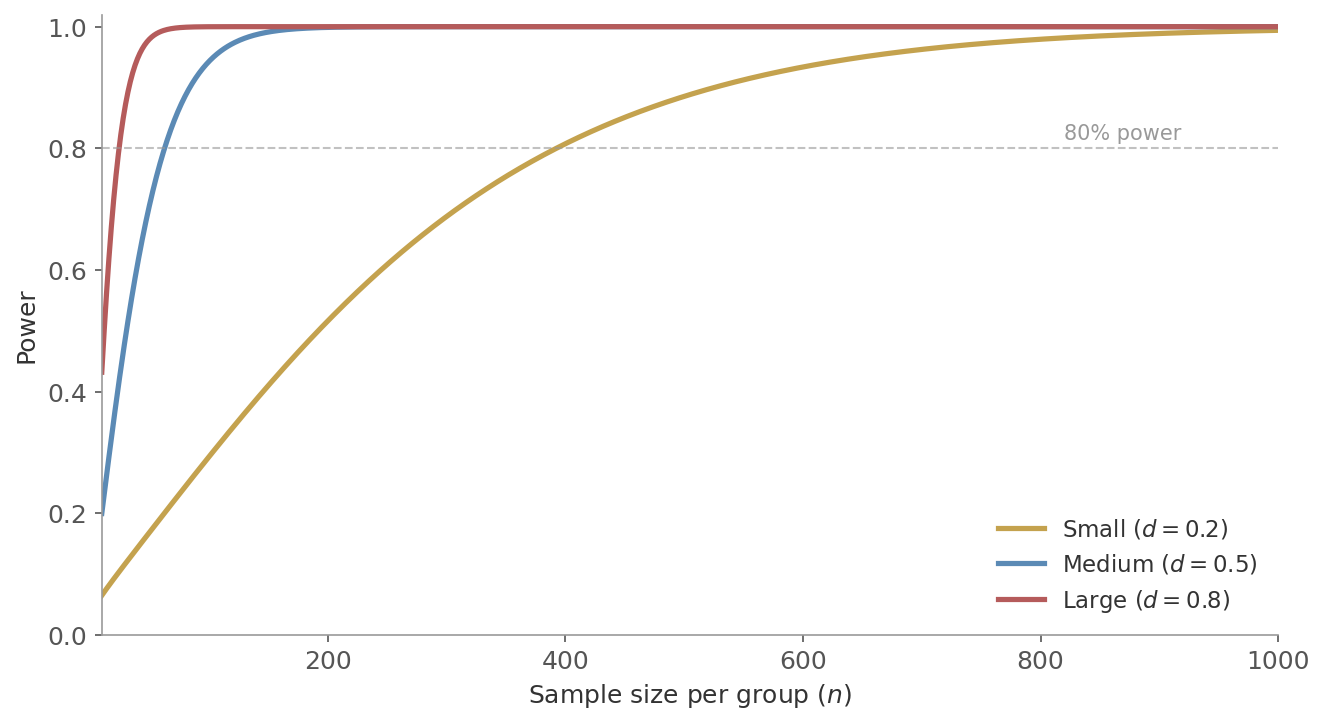

Figure 5: Power as a function of sample size per group, for three effect sizes ($\alpha = 0.05$, two-tailed). Large effects ($d = 0.8$) reach 80% power with under 30 per group. Medium effects ($d = 0.5$) need around 65. Small effects ($d = 0.2$) need about 400. The curves flatten as they approach 1.0 - adding more data has diminishing returns once power is already high.

Figure 5: Power as a function of sample size per group, for three effect sizes ($\alpha = 0.05$, two-tailed). Large effects ($d = 0.8$) reach 80% power with under 30 per group. Medium effects ($d = 0.5$) need around 65. Small effects ($d = 0.2$) need about 400. The curves flatten as they approach 1.0 - adding more data has diminishing returns once power is already high.

Putting It Together

These concepts form a pipeline. In practice, this is exactly how an A/B test works:

- State the hypotheses - what effect are you looking for?

- Choose $\alpha$ - how much false positive risk are you willing to accept? (Usually 0.05.)

- Choose power - how important is it not to miss a real effect? (Usually 0.80.)

- Define the MDE - what’s the smallest effect worth detecting?

- Compute sample size - how much data do you need?

- Run the experiment and compute the test statistic and p-value.

- Decide - reject or fail to reject. Report the confidence interval.

| Term | What it means |

|---|---|

| Significance level $\alpha$ | False positive rate - probability of rejecting a true null |

| $\beta$ | False negative rate - probability of missing a real effect |

| Power | Detection rate - probability of catching a real effect |

| p-value | How surprising the data is if there’s no effect |

| Effect size | Standardised magnitude of the difference |

| Confidence interval | Range of plausible values for the true parameter |

Next up: A/B Testing - designing, running, and analysing experiments.